“Capability to Maintain Buildings Metrics” Bulletin March 14 & 15

Capability to Maintain Buildings Metrics

The 4th Viability Metric assesses our Capability to Maintain Buildings throughout Whatcom County.

The following data points will be included:

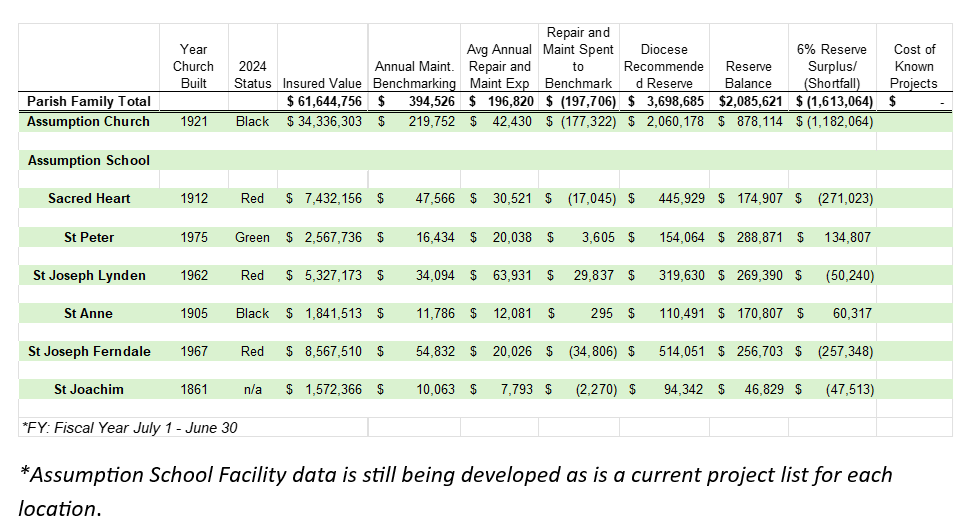

• Number of buildings and their condition status: The Archdiocese of Seattle conducted facility assessments in 2024 and classified each structure with a color coding. Black status (facility with at least two critical structures that need addressing) Red status (facility with at least one critical structure that needs addressing) Yellow status (repairs needed but not in critical condition) Green (no major needs at this time).

• Insured value of buildings: this provides some sense of the value of the buildings. It also reflects an approximate replacement cost of each property.

• Total maintenance spending to insured value: This measures total dollars spent annually on maintaining buildings and related systems compared to insured value. A ratio of at least 0.64% represents a parish family that budged adequate funds to maintain the property and should be the goal for this metric. For instance, if a parish family has $10,000,000 in total building insured value, they should be spending at least ($10,000,000 + 0.0064) $64,000 on maintenance annually.

• Ratio of PRF to insured value: This is the ratio of PRF savings (parish revolving fund) for the parish family to the insured value of the buildings. A low ratio of PRF savings to insured value is indicative of a lack of ability to cover the building maintenance expenses needed. The goal is for the PRF balance to be more than 6% of the value of the insured buildings. For instance, if a parish family has $10,000,000 in total building insured value, they should have at least ($10,000,000 * 0.06) $600,000 in their PRF savings account.

The Seattle Archdiocese’s 2024 evaluation of Whatcom County Catholic church facilities, as summarized in the table above, indicates that most locations fall short of recommended benchmarks for annual maintenance spending and reserve balances. (It should be noted that in the intervening months since 2024 projects have been completed that could improve the original assessment of buildings.)